Constellation Software (CSU): Is it really an AI loser?

30% a year for 20 years, but it's now down -50%. What's going on?

Disclaimer: This write-up is solely for informational and educational purposes. Always do your own research and invest at your own risk. This is NOT a buy or sell recommendation - and it’s purely my own opinion.

Besides, why would you listen to a random guy on the Internet?

Can you believe it… the last time I sat down and wrote a proper analysis piece on Substack was on Meta Platforms, back in 2022. That was more than four years ago.

Today, I’m back writing about a company I’ve recently become quite absorbed in. The company in question is Constellation Software Inc. (CSU for short). Depending on which part of the market you’re fishing at, you might or might not have come across this name because it’s not so ‘Main Street Popular’. And yet, since its IPO in 2006, the stock has compounded at roughly 30% per year, for nearly two decades.

I’ve also been exchanging notes on this with someone in my circle who has been studying the business closely, and some of what he shared with me is worth passing on before we go any deeper. On how the company allocates capital, he put it this way:

“No buybacks, still think acquisitions are more accretive after the crash. No stock-based compensation. Ownership is bought at market prices. Acquisitions IRR modelling doesn’t allow for synergies. Every shareholder letter talks endlessly about how they only care about IRR. No centralised HR or IT function. There’s no career page on the website. Managers who want to hire need to do it themselves. Everyone accountable to their own P&L.”

That’s a level of decentralisation that most organisations would find deeply uncomfortable, and it’s entirely by design. He also gave me a line that captures the stickiness of the software these businesses sell:

“I reached out to a friend who works at a top insurer in Singapore. They’re revamping their IT systems, wanting to do things in-house. I asked if the core policy administration system was being changed. Nope. Still there after at least 15 years. It’s actually a painful software. But it’s so vertically integrated and mission-critical that it’s never going away.”

But here’s the thing. A company that has compounded at 30% annually for 20 years is now sitting at its largest drawdown in nearly two decades. The stock has fallen more than 50% from its peak, in roughly 18 months. And that is the issue I want to spend the rest of this piece trying to answer honestly.

For a start, let’s understand CSU’s background a little.

Why Constellation Software Exists

In the early 1990s, Mark Leonard (founder of CSU) was working as a venture capitalist. He had noticed something consistent across his firm’s portfolio: the VMS (Vertical Software Market) businesses; the ones writing software for specific, narrow industries like transit scheduling, marina management or cemetery operations were producing returns that were disproportionately good compared to the headline technology investments everyone found exciting. They had loyal customers, recurring revenue, and almost no competition within their niche.

Source: Jeroen Coelen’s Linkedin

But there was a structural problem. Venture capital funds are designed to exit. You raise money from pension funds and institutional investors, you find promising companies, and after roughly five to seven years you sell your position and return the capital. For most VC investments, that model makes sense, you’re backing a bet on a technology or a market, and you exit when you’ve validated or disproved the thesis. But for these small VMS businesses, selling was economically irrational. These were businesses with annuity-like revenues and customers who almost never left. Selling them after a few years was like killing a golden goose because someone offered you a good price for the eggs.

Leonard’s founding insight shaped in part by reading Warren Buffett’s letters, which a mentor had introduced him to, was that these businesses deserved a permanent owner. Not a financial buyer who would hold for five years, extract value, load the business with debt, and sell it to the next buyer. A permanent owner who would run them indefinitely, let them compound their cash flows quietly, and then redeploy that cash into buying more of the same kind of business.

In 1995, he raised CAD 25 million from a single institutional investor and set out to build exactly that. He named the resulting company Constellation Software, an oblique reference to the idea that each acquired business would remain its own independent entity, a star in a constellation rather than a cog in a machine.

Why the Market is Currently Punishing This Business

Two distinct fears converged on CSU between mid-2025 and early 2026.

The first is the leadership transition. On September 25, 2025, Mark Leonard resigned as President for health reasons with immediate effect. Mark Miller, who has worked within the CSU organisation for over 30 years and co-founded the very first company CSU ever acquired back in 1995, stepped in. Shortly after, Leonard announced he would not stand for re-election to the Board, with his term ending at the May 2026 annual meeting, though he will remain involved as an advisor.

For a business where the founder’s intellectual framework (his specific approach to valuing companies, his insistence on permanent ownership, his discipline around return hurdles, his carefully constructed incentive architecture) is essentially the product.

This was not a planned, gradual handover where Leonard spent years grooming a successor and stepping back slowly. It was immediate, driven by health, and it left the market recalibrating almost overnight. Even if you trust the culture he built and the systems, he put in place, that kind of abrupt transition leaves a question mark that takes time and evidence to erase.

The second is artificial intelligence. CSU owns over 1,000 software businesses, many of which run on code that looks, like it was written in the 1990s. The generative AI narrative is that lower software development costs now mean new entrants can build competing products cheaply enough to undercut CSU’s businesses on price, which would erode the competitive advantages that underpin the entire portfolio.

CSU’s management held a special investor call to address these concerns, a remarkable step for a company that famously stopped doing quarterly earnings calls in 2018 and has historically communicated almost exclusively through annual shareholder letters. The market found the response unsatisfying because they were honest: it was too early to tell exactly how AI will affect their businesses.

The Business Model

The Market Failure CSU Was Built to Exploit

There are tens of thousands of software companies globally that serve very specific industry niches. The software that manages permit applications for a mid-sized city. The system that schedules shifts for a moving company with twelve employees. The tool that manages inventory for a regional marine equipment supplier. The platform that handles billing for a chain of dental clinics.

These are real businesses with real customers, real recurring revenues, and often very strong profit margins. Their customers depend on them daily and are almost impossible to displace once installed.

But they share one characteristic that makes them structurally orphaned from mainstream capital markets: their total addressable market (meaning the total pool of potential customers they could ever sell to) is tiny. Often just a few million dollars of annual revenue across the entire possible market. There will never be a second major player in cemetery management software in the Pacific Northeast.

So, these businesses sit quietly generating cash, often run by founders who have been building them for twenty years and have no obvious path to selling. They have essentially no competition within their niche.

Leonard’s insight was that this market failure was a persistent, exploitable opportunity. The businesses were not glamorous, and not growing quickly. But they were generating reliable cash, they had customers who were not leaving, and nobody wanted to buy them. He built a machine to acquire them systematically, operate them permanently, and use their combined cash flows to buy more of the same.

What made that insight durable was that acting on it required building an acquisition infrastructure; a relationship database of 200,000 potential targets, teams of specialists who had spent years cultivating relationships with specific founders, a standardised process for evaluating and pricing deals that takes decades to construct and cannot be replicated quickly. By the time other investors recognised the opportunity and started building similar structures, CSU had a 20-year head start on relationships, data and reputation.

Why the Economics Work for CSU

Before explaining how CSU extracts value, it is worth pausing on why the key measure (Return on Invested Capital, or ROIC) matters at all to an investor.

: Definition, Calculation, Importance & Limitations")

ROIC simply asks for every dollar of capital CSU puts into a business, how many dollars does it get back over time. The reason ROIC matters so much for a company like CSU — more than revenue growth, more than margins in isolation — is that CSU’s entire purpose is to take cash from one set of businesses and reinvest it into new ones. If the reinvestment keeps happening at high returns, the whole portfolio compounds.

Now, how does CSU achieve the high returns it targets?

Consider a typical acquisition: a VMS business generating roughly CAD 3 million in annual revenue, with approximately one-third of that as profit before interest and tax. CSU pays roughly one to two times annual revenue — so somewhere between CAD 3 and 6 million. After tax, the business generates somewhere around CAD 750,000 to CAD 800,000 in annual cash profit on that investment. That is a starting cash-on-cash return of 13-25%, before any operational improvements.

Now factor in what happens over time. The customer base barely churns; the most common reason customers leave is that their own business closes. Prices can be raised modestly each year because the software represents a tiny fraction of the customer’s total costs, so they have very limited incentive to switch even when prices go up. The software itself requires very little capital to maintain, so almost every incremental dollar of revenue the business generates flows straight to the bottom line.

Hold the business for seven years. The cumulative earnings have returned the entire purchase price. From year eight onwards, what CSU originally paid is already recovered, and the business continues generating cash indefinitely. The ongoing capital requirement drops to near zero and the reported return on that remaining invested capital becomes very high.

This is the unit economics case for why CSU’s model generates persistently high returns, because the underlying businesses are structurally positioned to generate reliable cash at very low ongoing capital cost.

How they defend their value proposition

VMS software does something that horizontal software (the kind that works across any industry, like Microsoft Excel or Salesforce) does not. It integrates into every operational layer of its customer’s business simultaneously.

Think about what a transit authority’s bus scheduling software does. It is not just a calendar application. It holds every driver’s credentials, shift rules, union contract constraints and time-off history. It maintains the maintenance record of every vehicle, including when each one is due for service and what work it has had done. It connects to the payment system that processes passenger fares, generates the reports that the authority files with the government, and feeds data into the payroll system that pays the drivers. Over years of operation, it has been customised to reflect that specific city’s specific rules, constraints and history.

Software academics describe this structure using three layers. At the bottom is what they call the System of Records, the database that is the source of truth for all of the operational data described above. In the middle sits the Business Logic layer, which governs how that data gets processed and what happens when different conditions are met. At the top is the User Interface — the screens that employees actually look at day to day.

CSU’s VMS businesses own all three layers. This is the structural fact that makes the AI disruption argument weaker.

An AI-native competitor trying to displace that transit authority’s scheduling software can only enter from the top, through a new interface or a new application. But the new interface is worthless without access to the System of Records sitting underneath it.

Every meaningful action the AI product would want to perform; reschedule a driver, flag a vehicle for maintenance, generate a regulatory report requires querying data that lives inside the incumbent’s system. The competitor either integrates with the incumbent, in which case the incumbent captures the value of the improvement, or it tries to build its own System of Records from scratch, which means convincing the transit authority to migrate years of operational history, retrain its workforce, accept the risk of downtime and data loss, and gamble the operation of a public service on untested software.

For a software product that represents (usually) a low, single digit % of the authority’s total operating budget and works reliably every single day, there is almost no scenario in which that risk is worth taking.

The appropriate question for an investor today: is there any evidence that this dynamic is changing? Are CSU customers churning at higher rates than historical levels? Are any of the 1,000+ portfolio businesses reporting competitive pressure from AI-native entrants?

For now, the last two quarters earnings don’t support this narrative, but since the stock market is forward-looking, we’re pricing in that range of outcome.

A subtler version of the AI concern is seat compression: not that the software gets replaced, but that artificial intelligence tools reduce the number of people who need to use the software, meaning fewer licences are sold. But even here, the businesses most exposed to this risk have strong structural incentives not to reduce headcount even when technology enables it (especially in the public sector). A government transport department that reduces its employee count by 20% because of AI saves money but also loses political support. The incentives cut both ways.

A short AI Detour

And since we’re already on this topic of AI, I came across this perspective from Mohnish Pabrai (a billionaire investor), where he expressed a slightly contrarian take about AI’s impact on CSU.

/ Posts / X")

His core argument is that the market has it backwards. He thinks that the incumbents are more likely to benefit from AI as a cost reduction or feature enhancement tool, while new entrants still face the same fundamental barriers they always have. Business rules, compliance logic, and user experience built up over decades do not become easier to replicate just because code generation got cheaper. Code generation was never the main cost of writing and selling software in the first place.

AI anxiety among founders may accelerate deal flow for CSU. If a founder running a small VMS business is nervous about what AI does to their competitive position, they may be more willing to sell, and more willing to sell to a buyer with CSU’s track record and permanent ownership model. The fear that the market is pricing as a headwind could, in practice, be nudging more targets toward the negotiating table.

CSU maintains a database of roughly 100,000 vertical software companies in the US alone, and their teams are in contact with each of them at least twice a year, by phone and by email, with a message that is essentially the same one Warren Buffett has been sending to business owners for decades: if you ever decide to do something, think of us. If you assume that roughly 2.5% of founders between the ages of 40 and 80 exit the business each year through retirement or otherwise, that is around 2,500 companies naturally entering the pipeline annually, before you count anyone who simply decides the timing is right.

His overall read is that some of the current sell-off reflects irrational fear rather than fundamental deterioration. That is a contrarian position, and I am not saying he is definitely right. But it is a perspective that deserves to sit alongside the bear case, not be dismissed.

Industry and Competitive Dynamics

The VMS market is fragmented almost by definition. Because individual niches are so small, the entire opportunity is scattered across dozens of industries and hundreds of geographies.

Several acquirers have emerged over the past decade attempting to replicate CSU’s model. Chapters Group in Germany, Addtech and Halma in Europe, and a number of private equity firms focused on software all operate in adjacent space. The honest assessment is that they represent real competition for specific deals, particularly the cleaner, higher-margin acquisitions where the thesis is straightforward and multiple bidders can underwrite similar returns.

Where CSU retains an advantage is in the messier situations, the business with declining organic revenue, the founder who has let operational discipline slip, the company with unusual customer concentration. These require proprietary data from hundreds of comparable historical acquisitions to price correctly.

| Seeking Alpha")

The more important competitive dynamic is internal. CSU’s six operating groups — Volaris, Harris, Topicus, Vela, Jonas and Perseus — are competing with each other for the same acquisition targets. Each group maintains its own team of deal specialists who cultivate relationships with specific founders over multi-year periods. There are rules preventing one operating group from pursuing a target that another group is already in conversation with, unless there has been no contact for 12 months. This creates a system where good deal teams are rewarded with more capital, and complacent ones risk having their targets poached by a sister group.

The structural constraint worth examining honestly is that CSU is generating roughly CAD 1.7 billion in cash each year that it needs to reinvest into acquisitions. The VMS small-deal pipeline — businesses acquired for under CAD 5 million — has historically absorbed most of this. But at current scale, even running 100 acquisitions per year at an average deal size of CAD 5 million, that is only CAD 500 million deployed. Something has to absorb the rest, and the logical answer is larger deals which CSU has been increasingly pursuing, and which carry different risk characteristics than the traditional small VMS playbook. This tension between the capital being generated and the opportunity set available to absorb it is the central mechanical challenge the business faces.

On CSU’s capital allocation

Most investors who follow software companies are familiar with Free Cash Flow, typically calculated as operating cash flow minus capital expenditure, the cash a business generates after spending what it needs to maintain and grow its operations. Many companies adjust it, adding back stock-based compensation or other non-cash charges to make the number look better.

CSU uses a different measure: Free Cash Flow Available to Shareholders, or FCFA2S. This definition is deliberately more conservative. It only counts what is genuinely available to equity shareholders if the company made no new acquisitions.

Why does this matter beyond technical accounting? Because the choice to measure performance this way, and to tie management compensation to it, reveals something specific about how Mark Leonard thought about his responsibilities. He was not trying to maximise the number reported in the headline. He was trying to measure the actual economic value being created for the people who owned the business. The name itself — “available to shareholders” — is a steward’s framing, not a manager’s framing.

This mentality shows up in everything else about the business. He never issued share-based compensation. He required executives to buy stock with their own cash. He stopped taking a salary in 2015 because he felt he had enough personal wealth and did not want to, in his words, “freeload” on CSU shareholders.

All of this context matters now because the question being asked by the market is whether Mark Miller will operate with the same intellectual honesty and the same long-term orientation. Miller has explicitly stated that PEMS (Permanent Engaged Minority Shareholder) investments — the new strategy of taking minority stakes in larger public companies — are being evaluated against the same return hurdles as traditional VMS acquisitions. The test is whether it stays the right answer when the deals get harder to find and the pressure to deploy capital increases.

The Three Mechanisms

Beyond culture and character, three specific institutional mechanisms are what keep CSU’s capital allocation honest.

The first is the Post-Acquisition Review, or PAR. Every acquisition is formally evaluated one year after it closes, comparing what the deal team projected against what actually happened. Crucially, if a deal underperforms, the shortfall stays permanently in that manager’s capital base. The manager who underwritten an optimistic assumption lives with its cost in their return metrics for as long as they manage that business. This creates an internal market for honest underwriting.

The second is what Leonard called the magnetic effect of hurdle rates. When CSU has historically lowered its required minimum return on an acquisition, its Internal Rate of Return, or IRR, hurdle, which represents the minimum annualised return it requires before it will do a deal, the effect was not limited to the marginal deals at the boundary. The average return across all deals done after the rate change declined toward the new threshold. The explanation is behavioural: once a lower standard is acceptable, deal teams negotiate to it. They stop pushing sellers as hard on price. They become more willing to accept an uncertain recovery plan because the bar for what counts as acceptable has moved.

The third mechanism is the Keep Your Capital directive. When a business unit is generating strong returns on its existing investments, headquarters can instruct it to retain capital and reinvest locally rather than sending it up the chain. This prevents the distortion that can occur when older, fully recovered acquisitions report very high ROIC which can inflate bonus pools and create perverse incentives. Keeping capital at the level where the best opportunities are identified maintains the quality of the deployment.

What Miller Has Done So Far

Miller’s most significant early action has been introducing the PEMS. Rather than acquiring companies outright, CSU takes minority stakes in larger public companies; the first meaningful example being a 12.7% stake in Sabre Corporation, a US travel technology company. This comes with governance rights, including a seat on Sabre’s board.

Larger private acquisitions are possible but increasingly competitive. Public companies at distressed valuations represent an alternative pool of capital deployment that is less competitive precisely because most acquirers want full ownership, not minority stakes with influence. Leonard apparently helped develop the approach and assisted with the Sabre deal before his departure.

Whether PEMS can actually deliver the same economics as the traditional VMS machine is unknown. The Sabre investment is too recent to evaluate. What is observable is that Miller framed it correctly, as an extension of capital allocation discipline into a new format, not as a pivot away from the core strategy.

CSU Financials

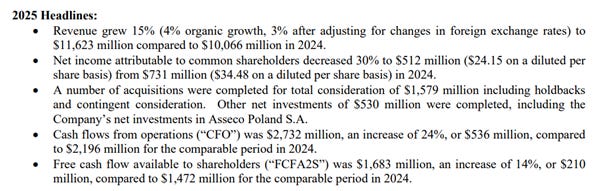

The 2025 full-year results tell the story of a business that kept working while its stock fell in half.

Revenue grew 15% to CAD 11.6 billion. The portion of that growth that came from existing customers was approximately 4%. When you strip out currency movements and look only at maintenance and recurring subscription revenue from existing customers, that organic growth was 6%. This is the number that should be most interesting, because it tells you whether the existing portfolio of 1,000+ businesses is healthy. A 6% growth rate from existing, sticky customers suggests pricing power is intact and the feared AI-driven churn has not materialised in practice.

On FCFA2S, the full year came in at CAD 1,683 million, up 14% from CAD 1,472 million in 2024. So why did the stock drop on earnings? The headline earnings per share came in at CAD 25.10 versus an estimated CAD 38.48. That looks alarming. But to understand why it happened, you need to understand how accounting treats acquisitions.

When CSU buys a VMS business, it does not simply record the purchase price as an asset and move on. Accounting standards require it to allocate the purchase price across the specific assets and contracts it acquired; customer relationships, software licences, brand value, and so forth. These allocated values then get amortised through the income statement over several years, showing up as an accounting expense even though no cash is leaving the business. The larger and more frequent the acquisitions, the bigger this non-cash accounting drag on reported profits.

One number from 2025 deserves specific attention and honest acknowledgement of uncertainty. The ratio of capital CSU reinvested in acquisitions divided by FCFA2S — a measure of how aggressively it is redeploying its cash — appears to have declined from over 100% in prior years to approximately 90% in 2025.

Finally, the initial cash return on the 2024 acquisition cohort appears to be tracking lower in its first year than historical norms. One explanation (consistent with CSU’s own stated strategy) is that they deliberately acquired sub-optimised businesses that require 18-36 months of operational improvement before generating their full earnings potential. This is a normal feature of the model. The alternative explanation is that, facing pressure to deploy larger amounts of capital, CSU has been accepting lower projected returns at the deal stage. Both explanations are consistent with the current data. (as crunched by “The pursuit of compounding”)

The difference between them will only become visible over-time as we monitor how they optimize and generate returns over the next two years.

Looking at their valuations today

At CAD 2,464, CSU’s total market value is approximately CAD 52.2 billion (~$38.3B). The 2025 FCFA2S was US$1,683 million. That puts the multiple at approximately 22.8 times FCFA2S. To understand whether this is cheap or expensive, the question is: what growth rate has to be true for that price to represent good value?

The simple arithmetic:

At 23x FCFA2S, the cash yield to shareholders — ignoring growth entirely — is roughly 4.3%. To earn 10% annually on the investment, you need the rent to grow by 5.4% per year on average. CSU’s FCFA2S has grown at 24% per year over the past five years. Even if growth decelerates sharply toward 8% going forward, the arithmetic still delivers acceptable returns at the current price.

The main challenge investors are currently grappling with is… how reliably can we expect them to grow FCFA2S from here given all that we’ve discussed till date?

The range of outcomes:

FCFA2S grow 10%, ending multiple of 15x (continued compression),

the 5-year-CAGR would be ~1.2%

FCFA2S grow 15%, ending multiple of 20x (stay here),

the 5-year-CAGR would be ~12.1%

FCFA2S grow 20%, ending multiple of 25x (expand a little),

the 5-year-CAGR would be ~22.3%

CSU has historically traded at 40x to 50x FCFA2S during periods when it was growing that same metric at 25% to 40% annually. Today, it is sitting at roughly 23x — a multiple that already prices in meaningful doubt about the business.

That is the trade-off worth being honest about. The range of outcomes we looked at shows that the bear case is not really about the business deteriorating. A 10% FCFA2S growth scenario is still a functioning, cash-generating machine. What kills your return in the bear case is multiple compression.

The base and bull cases show what happens when that narrative simply fades. You do not need CSU to re-rate back to 40x or 50x. You just need the market to stop actively discounting it. At that point, even modest multiple expansion from 23x toward 25x, combined with 15% to 20% FCFA2S growth, gets you into the range of 12% to 22% annually.

(and in full disclosure; Yes, I do have an existing position in CSU as of the time of this writing)

Love,

Chi Keng

Disclaimer: Do not interpret anything above as financial advice. As of the date the Report is published, the Author may or may not hold a position in the security mentioned. Nothing in this Report constitutes investment advice. Readers should conduct their own due diligence and research and make their own investment decisions. This is NOT a buy or sell recommendation.